Don’t Underestimate This Crucial Key to Building Wealth

As the deadline for making 2016 annual contributions to IRAs and Roth IRAs approaches (April 18, 2017), it’s the perfect time to outline best practices for saving.

How do you know if your saving strategy is solid? Consider these 5 pillars for success:

1. You’ve started

There’s no way around it: with ample time, compound interest is magical. With little time, it’s tyrannical. The earlier you start saving, the better. This is arguably the best financial lesson anyone can teach their child.

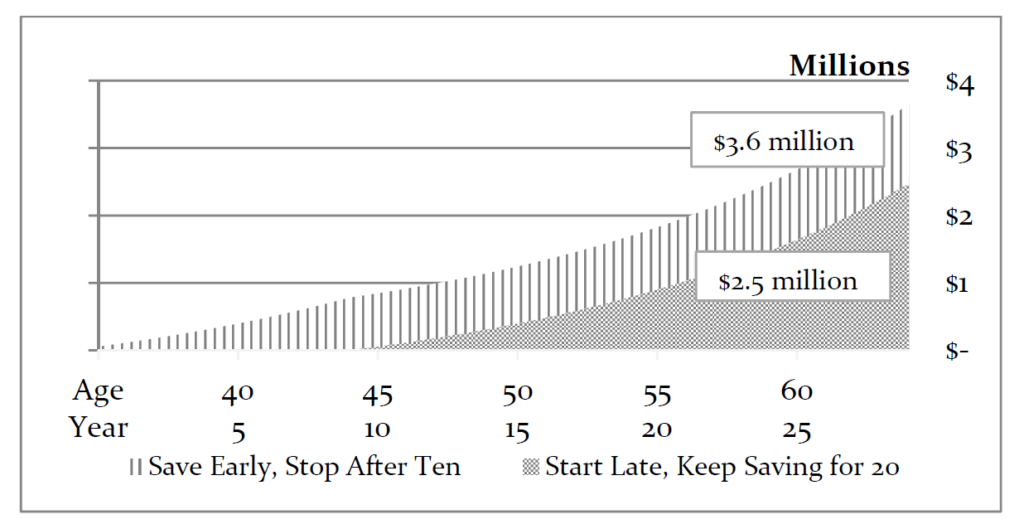

For late starters, saving to meet retirement goals can become something like a matter of brute force. Consider the following graphic (assuming gross income of $250,000, savings of $50,000 per year, investments returns of 8% per year, and ignoring both inflation and potential tax effects).

The late saver can never catch up to the early saver, despite saving longer and putting away more dollars.

2. You’re saving at the correct rate

Whether the stock market goes up or down is out of your control. Knowing whether your savings rate is correct (whatever the goal or goals) is all about running the numbers.

When it come to your retirement goal, you should be fluent in answering the following questions:

How many years must I continue to work at my current savings rate?

If I save 2% more, how does that change my retirement timeline? How about 5% or 10%?

For most of the investors we serve, we recommend saving at least 20% of annual income, for retirement planning, well above what the average American saves.

But, like most aspects of your financial plan, your savings rate must be customized to you. You advisor can help you decide how much to save, what vehicles to use, and whether or not debt paydown should be a prioritized form of saving for you.

With ample time, compound interest is magical. With little time, it’s tyrannical.

3. You’ve automated your saving strategy

Saving, like dieting, is hard. We may be programmed to store fat in our bodies, but when it comes to money, we’re wired to display our status within the tribe. That can be expensive.

Because spending is so easy, it’s wise to use any means at your disposal to pay yourself first. Automatic payroll deduction is a saver’s best friend, and employer-based or self-employed retirement plans become the cornerstone of success for many wealth builders. Not only can automatic deductions from your paycheck make the task of saving seem effortless, there is free money in the employer match (if it’s available), and your savings grow tax-free.

And you don’t have to stop there. You can establish automation beyond your work-related plan for any number of goals.

4. Your debt-to income ratio is healthy

Your debt-to-income ratio compares the amount of debt you’re carrying in relationship to the amount of money you’re bringing in. A regular review of these numbers should be with the goal of keeping what you owe from crowding out your ability to save at your correct rate. Also, it must be said: each of us should avoid credit card debt like the plague.

5. Your saving strategy is tax aware

For most of us, saving in a tax-aware manner means contributing to a pre-tax retirement savings plan. You (and your spouse, if you’re married) should always maximize your pre-tax savings first. Only consider after-tax savings if you have already maxed out your pre-tax retirement plans, and if you already have your insurance protections and emergency fund in place.

Cover these bases with the help of your financial professionals and review them each year to stay on track. On your path to building lifetime wealth, never lose sight of the fact that your saving strategy is at least as important as your investment plan.

By Joan Hill, Communications Coordinator

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by TGS Financial Advisors), or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from TGS Financial Advisors. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. TGS Financial Advisors is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of the TGS Financial Advisors’ current written disclosure statement discussing our advisory services and fees is available upon request.