The Election & Your Money

This was my eleventh presidential election, and surely the most contentious. We now know the outcome, which is disturbing to half the voting public, while not necessarily reassuring to the rest.

What are the investment implications of this election? How will the results affect our portfolios? Are there actions we should take, now that we know the result, to improve our positioning? For more of our thoughts on this topic you can also watch a recording of our recent webinar, The Markets & the Election Season.

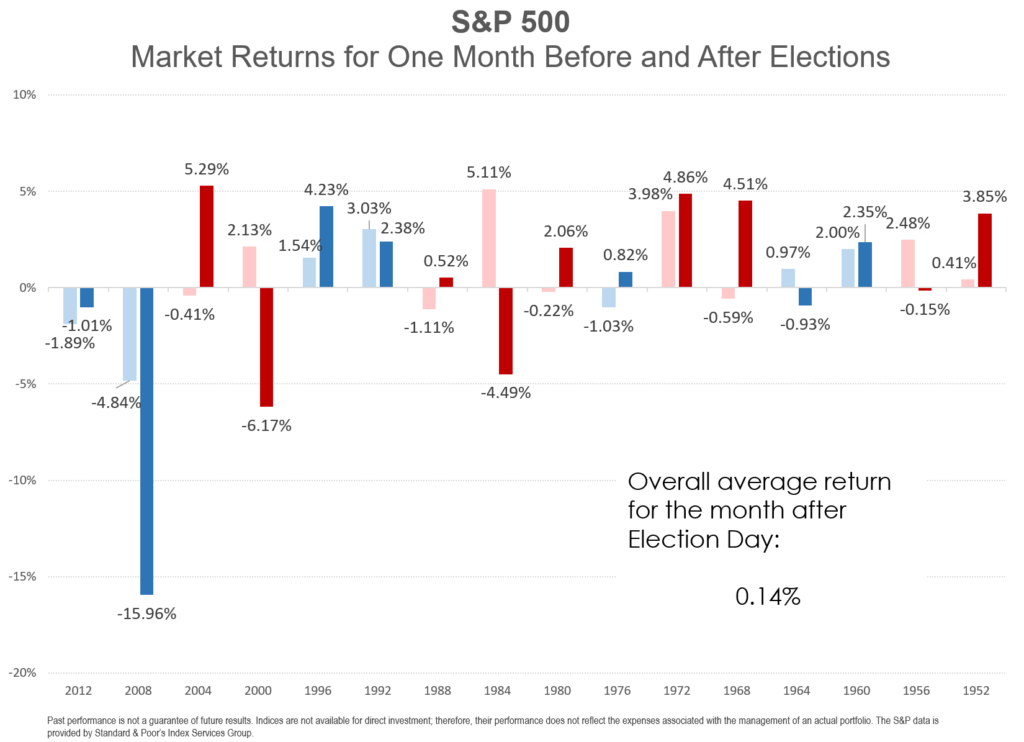

As always, let’s start by examining the data. We have really good data going back to the presidential election of 1952 about how U.S. financial markets have reacted in the short-term, over the two months on either side of presidential votes, to different election outcomes. Let’s see if we can apply these in light of Tuesday’s result.

Here’s a summary of some of the key points (with comments on the actual election results):

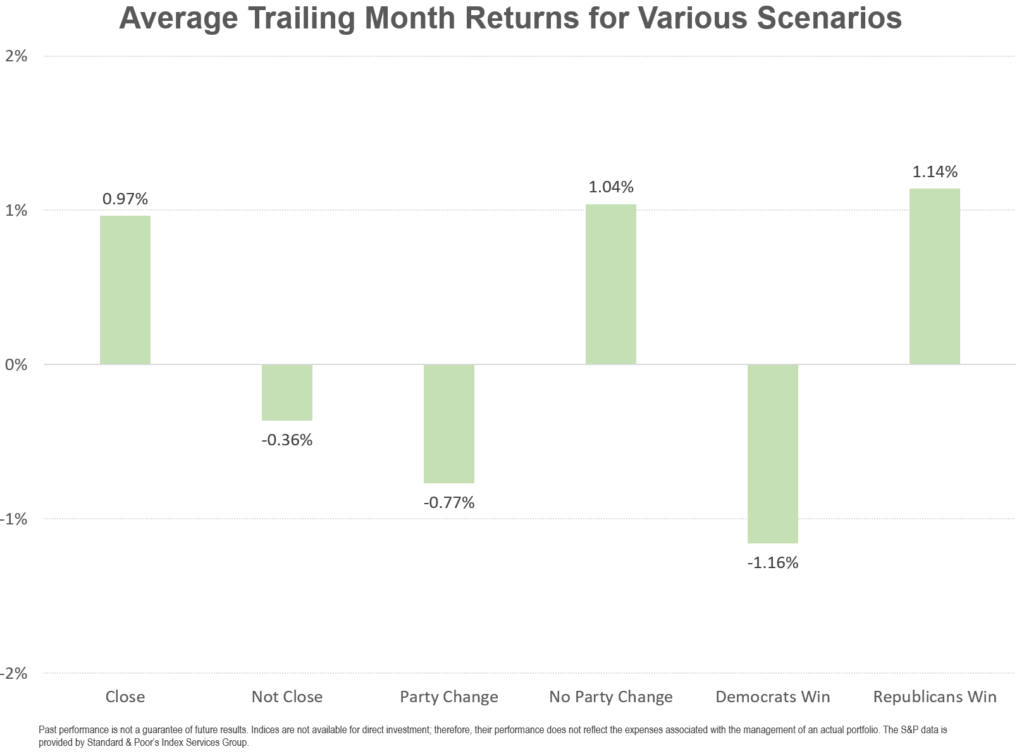

• Markets usually go up slightly in the two months bracketing the presidential election. (Yep.)

• They go up more if the election is close. (Incredibly close, and the market has rallied.)

• If the election is a landslide, they go down a bit. (Nothing to see here.)

• If the party in the White House changes, they go down. If the White House remains with the same party, they go up. (Suggests a dip.)

• If a Democrat wins, markets decline, while a Republican victory sends markets up by exactly the same margin. (A Republican, of sorts, so a rise.)

• None of these historical moves averages as much as 2% in either direction. (We’ve already seen a greater move, in both directions, both before and after.)

So the best scenario for the markets would have been for the Democrats to retain the White House by a slim margin, and a Republican to win the presidency. Which is clearly self-contradictory, and thus no help at all. At this point, the markets have panicked at Trump’s victory, then rallied sharply. So a variety of indicators of limited utility have already been overtaken by events. Too late to panic, too late to celebrate.

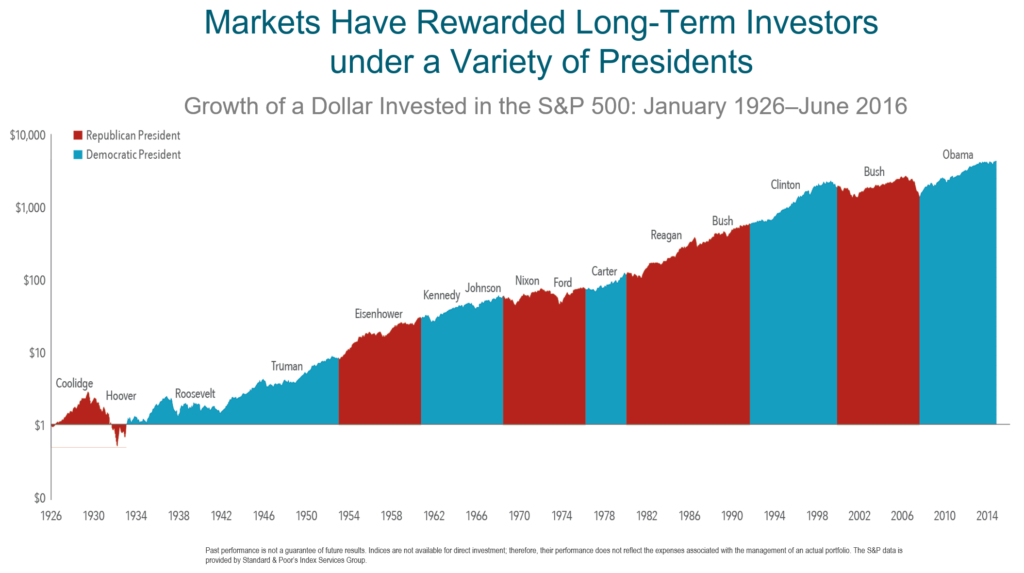

Does either party have a longer-term advantage? Yes, there is a slight advantage for Democrats in long-term returns. But if you deduct the market crash of 1929-1932, the Republicans have a slight edge. As investors, we really have no reason to expect a predictable advantage or disadvantage from Trump’s victory.

Let’s look at a much more reliable and actionable metric.

As we often do, we fall back on valuation. Economist Robert Shiller of Yale University won the Nobel Prize in Economics for his insight, captured in the Shiller CAPE (Cyclically-Adjusted Price Earnings ratio), that when stock market valuations are high, future returns are lower, and when valuations are low, future returns are higher.

The last two times the presidency changed hands, in 2000 and 2008, we used Shiller CAPE to inform our broad perspective on the markets.

In 2000, when George W. Bush finally won, valuations were high, and we warned that risks were high and prospective returns likely to be low. We took a defensive posture. As the tech crash continued through 2003, our portfolios largely avoided the market decline.

In 2008, when Barack Obama won a compelling victory in the midst of the worst stock market decline since the Great Depression, we observed that stock prices were below average. With risks lower and opportunities higher, we pounded on the table in favor of buying stocks. At the market bottom in 2009, our stock holdings were the highest ever. We were ultimately well-paid for owning stocks, as Barack Obama’s first term was one of the most profitable for U.S. stock market investors in a generation.

As investors, we really have no reason to expect a predictable advantage or disadvantage from Trump’s victory.

On the Friday before the election, market prices were high. Before the vote, Shiller CAPE was at 26.5 times trailing earnings, putting us in the top 7% of historical valuations (93.4 percentile). After the Wednesday, November 10 rally, we hit 27.5 times trailing earnings and the 95.2 percentile. (In other words, the market has been this expensive less than 5% of the time since 1926.) Based on this price increase we will slightly increase our cash position. This will make our portfolios even more defensive, just as they were in 2000 when Bush 43 was elected.

There is an aspect of our portfolio strategy that may intersect in interesting ways with the election results. While U.S. valuations are very high, all foreign stock markets are cheaper as measured by CAPE, without exception. We are overweight foreign equities.

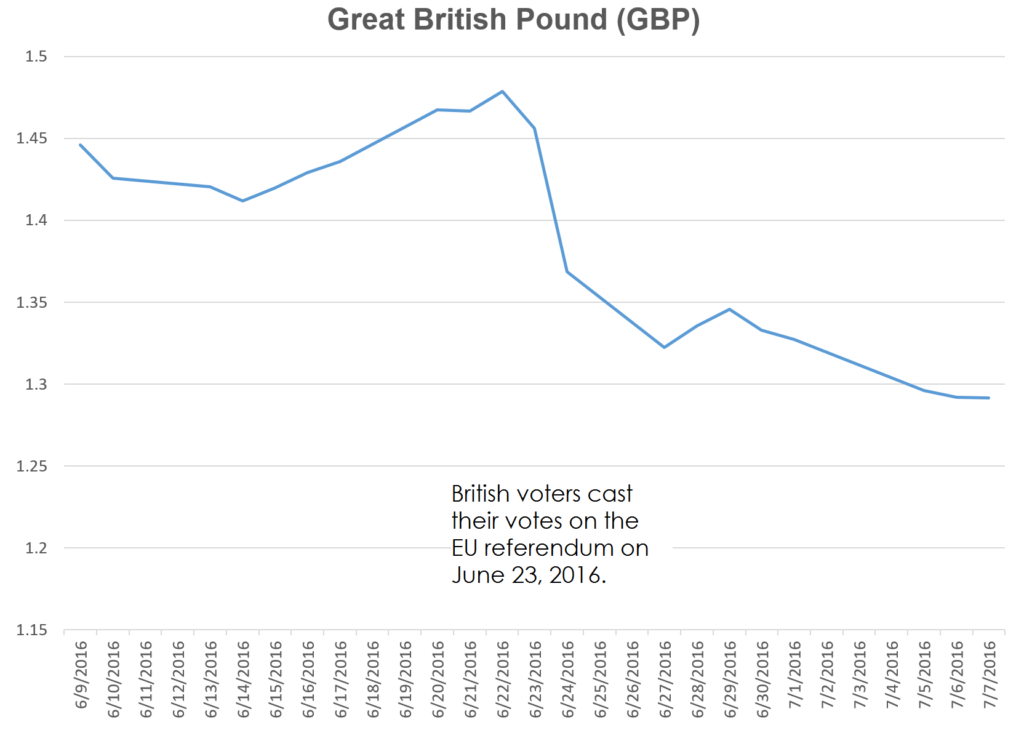

To evaluate how this positioning may perform in the coming years, let’s examine the reaction of markets to the British vote on whether to leave the European Union (Brexit). Immediately before the vote, polls predicted that Brexit would fail and Britain would remain in the EU. Markets rallied sharply. But Britons actually voted for Brexit, against polling predictions. Markets fell sharply, both in the U. S. and in Great Britain. But within weeks, markets fully recovered in both the U.S. and overseas.

One market that fell sharply and has continued to fall in reaction to Brexit is the currency market for the British pound, which fell by 6.0% the next day and has fallen another 10.4% since, with no sign of recovery.

This is an intriguing scenario given the Trump victory against the indications of the majority of polls. If election results followed the Brexit path, we would expect to see a sharp and persistent decline in the value of the U.S. dollar. That scenario would actually benefit our target portfolios, because we are strongly over-weight foreign equities. A falling dollar increases the price of foreign stocks. So far we see no such trend.

Between repealing and replacing Obamacare, deregulation, reforming the VA, and filling the empty Supreme Court seat, Trump already has a governing agenda that would challenge an FDR or Reagan. (I met Ronald Reagan, and Trump is… (you can finish the sentence as you wish.))

The long-term wild card around Trump’s election is protectionism. No president in more than a century has run on such an explicitly anti-free trade platform. Any move toward sparking a trade war could have a negative impact on both the markets and the real economy. This is an issue we’ll watch closely as we learn more about Trump’s legislative priorities and his choices for cabinet positions.

Know that our portfolios are defensive and diversified, that we have cash available to invest in the event of a large market decline, and that we remain committed to a global perspective on investing. As always, we are devoted to your lifetime financial success, and none of our personal political perspectives will ever deflect us from making decisions based solely on what we believe to be your best long-term interests.

So, turn off the cable news channels, hug your spouse and your children, take your dog for a walk, read a novel, or enjoy an adult beverage. We’re keeping watch.

By James S. Hemphill, CFP®, CIMA®, CPWA® / Managing Director & Chief Investment Strategist

Jim has been a CERTIFIED FINANCIAL PLANNER™ professional since 1982. Jim specializes in complex wealth transfer and retirement transition strategies and coordinates TGS Financial’s investment research initiatives.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by TGS Financial Advisors), or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from TGS Financial Advisors. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. TGS Financial Advisors is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of the TGS Financial Advisors’ current written disclosure statement discussing our advisory services and fees is available upon request.