Why We Prefer 529s Over UTMAs

There are several vehicles that can be used to save money for college, and each has its own set of rules and complexities. As it is with most financial topics, your options for education funding should be reviewed by your financial advisor before you make a selection. This article compares and contrasts a few characteristics of 529 plans and UTMA (Uniform Transfers to Minors Act) accounts and explains the reasons we generally tend to recommend 529s. UTMAs are the updated form of the previous UGMA (Uniform Gift to Minors Act) accounts. It is still common to see these acronyms lumped together. Both represent a type of custodial account.

For more information about these and other savings vehicles, or a detailed look at options for grandparents who wish to help with college funding, please click on the “read more” links that follow this piece.

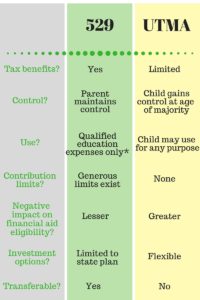

Here is a quick guide to some important differences between 529s and UTMA accounts.

Let’s take a closer look at the differences in the tax benefits and control parameters of these savings vehicles, as well as their impact on federal student loan eligibility.

Tax benefits

One could argue that the UTMA was designed for simpler times. It used to be that parents could use UGMAs (the older version) to move investment income out of their high tax bracket and into their child’s low bracket.

And then the federal “kiddie tax,” a tax on the unearned income paid to minors, was born. Today, in the 2016 tax year, the first $1,050 of earnings on UTMAs is federal tax free, the next $1,050 is taxed at the child’s rate, and above $2,100 the account’s earnings are taxed at the parents’ highest marginal tax rate. These tiers are subject to change, and things get more complicated when a child has his or her own earned income.

529 plans offer a huge tax incentive to those who save for college funding. Earnings in 529 plans grow tax free, and the Pension Protection Act of 2006 made this tax treatment permanent. Even when the money in these plans is taken out to pay for qualified education expenses, it is not taxed. Many states offer full or partial tax deductions or credits for 529 plan contributions, but contributions are not deductible on your federal tax return.

Control

A key to understanding the control parameters for UTMAs is in the name of the vehicle itself, specifically in the word “transfer.” (In the old UGMA, the key word is “gift.”) When parents establish a UTMA, they are giving the child the assets that are contributed to the account. While a custodian maintains control of the account in the case of minor children, the assets can only be used for the child’s benefit. When the child reaches adulthood, control of the account is completely and permanently transferred to him or her. Furthermore, even while the child is still a minor, contributions to the account are irrevocable.

Once control of a UTMA is transferred to the child, the assets can be used for any purpose.

The assets in a 529 plan, on the other hand, should only be used for qualified educational expenses. (Otherwise, the account owner forfeits the federal tax treatment.) The named beneficiary has no legal rights to the account, so if the child named in a 529 does not go on to college, the assets can be transferred to another family member, including a parent.

Bottom line, the donor is, and stays, in control of a 529.

Impact on financial aid

UTMA accounts are reported as student assets on the Free Application for Federal Student Aid (FAFSA). The 2016 financial aid formula stipulates that students must contribute 20% of their own assets before they can be eligible for financial aid. Thus, $10,000 in an UTMA will reduce eligibility by $2,000. This means that a UTMA can have a greater impact on financial aid eligibility than assets in parental accounts.

For this reason, the ideal conditions for the use of an UTMA include the certainty that your child will not be applying for financial aid.

In contrast, some parental assets are shielded from the financial aid formula, and others, such as 529 plans, reduce aid eligibility at a maximum 5.64% rate.

Read more

For a broader overview of the various ways to fund college education, including comparison charts, visit the Raymond James College Planning page.

To compare and contrast more features of 529s and UTMAs, visit this savingforcollege.com page.

To learn more about opportunities that grandparents can use to contribute to their grandchildren’s college fund, read this article by Michael Kitces.

By Joan Hill / Communications Coordinator

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by TGS Financial Advisors), or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from TGS Financial Advisors. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. TGS Financial Advisors is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of the TGS Financial Advisors’ current written disclosure statement discussing our advisory services and fees is available upon request.